Table of Contents

WalletConnect Pay and the Future of Web3 Commerce

Crypto has always promised a future where money moves as freely as information. Fast borderless and permissionless. Yet for all its technological breakthroughs, one core use case has remained frustratingly out of reach: real world payments.

For years, the idea of paying for coffee, groceries, or online services with crypto sounded exciting. But in practice it was messy. Wallet switching. Network confusion. Gas fees. Failed transactions. Delayed settlements. For both users and merchants, the experience felt anything but seamless.

The Rise of Stablecoins

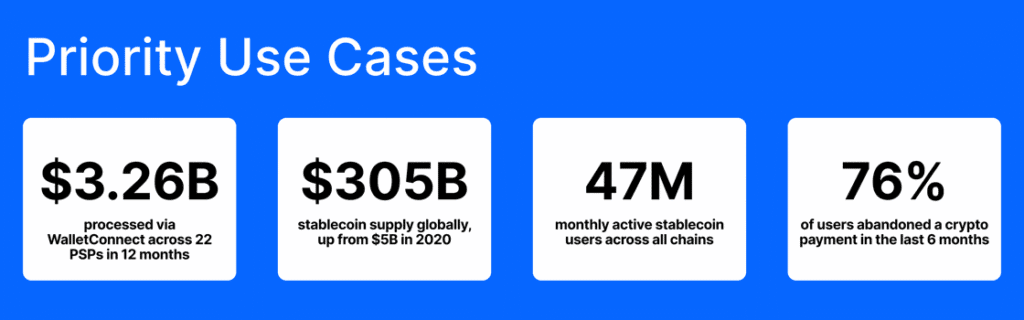

Stablecoins have emerged as the breakthrough solution. By eliminating volatility they unlocked practical use cases such as cross-border transfers treasury operations and remittances. According to Bloomberg stablecoin transactions reached $33 trillion in 2025 with projections suggesting volumes could climb to $57 trillion by 2030. This growth reflects real-world settlement activity rather than speculative trading, particularly in regions with unstable currencies or inefficient banking systems.

That is now changing.

WalletConnect Pay represents a structural shift in how crypto integrates with the real economy. Not as an experiment. Not as a niche feature. But as a fully functional, scalable payment infrastructure designed for everyday use.

This is not about adding another crypto payment button. This is about removing friction entirely.

The Core Problem Crypto Couldn’t Solve

The demand has always been there.

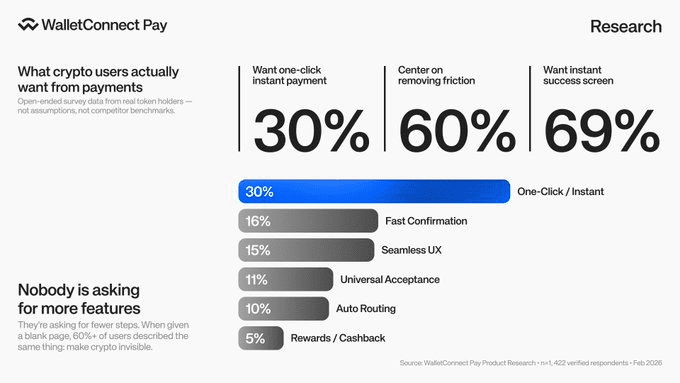

Most crypto users want to spend their assets. Data consistently shows strong intent toward real-world usage. But intent alone doesn’t create adoption. Execution does.

And execution has been the weak point.

Users faced:

- Confusing wallet flows

- Network mismatches

- Gas unpredictability

- Manual address handling

- Poor checkout experiences

Merchants faced:

- Volatility risk

- Compliance complexity

- Fragmented integrations

- Slow or uncertain settlement

Traditional payment systems, despite being expensive and slow, still won on simplicity.

Crypto needed to match that simplicity without losing its advantages.

Why Payments Still Lagged

Despite this surge crypto struggled at the checkout counter. Merchants faced fragmented wallets multiple blockchains and unclear regulatory frameworks. Consumers were forced to make technical decisions during transactions a barrier to mainstream adoption. Piggybacking on card rails through crypto debit cards or Google Pay integrations offered temporary relief but failed to deliver a truly new payment system.

WalletConnect Pay: A New Standard

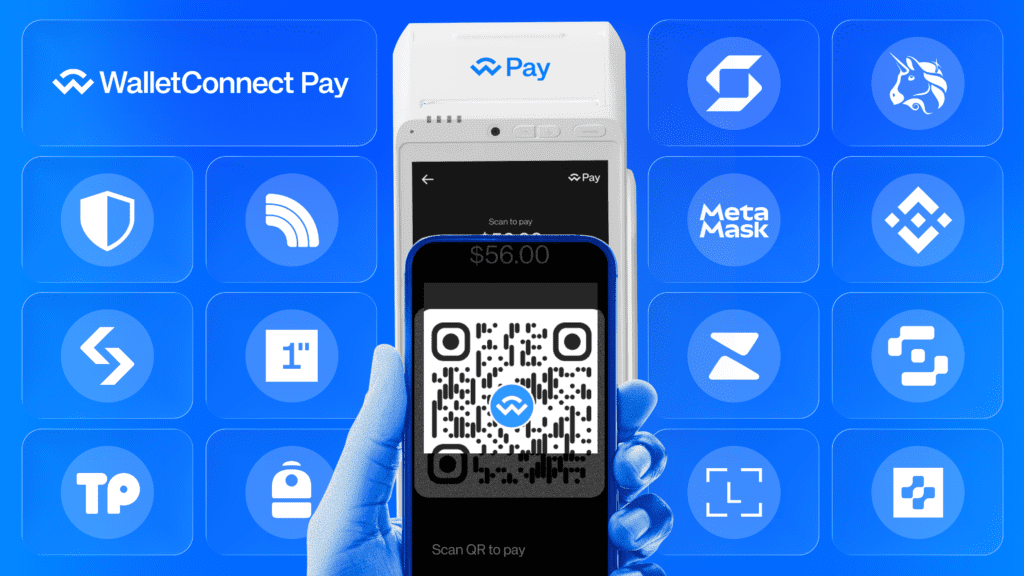

WalletConnect Pay addresses these challenges by standardizing wallet-to-merchant interactions. The result is a two-second checkout experience that requires no new hardware for merchants and no complex steps for users. Customers simply scan, approve, and continue.

In early 2026, WalletConnect partnered with Ingenico, enabling stablecoin payments across 40 million terminals in more than 120 countries. This integration means consumers can now pay with USDC, EURC, or USDT using popular wallets like MetaMask, Trust, and Safe directly at grocery stores, hotels, and gas stations.

WalletConnect Pay: The Structural Shift

WalletConnect Pay approaches the problem differently. Instead of forcing users and merchants to adapt to crypto, it adapts crypto to existing payment behavior. At its core the system introduces a simple but powerful concept:

Any wallet. Any asset. Any chain. One flow.

Users pay directly from wallets they already use. No new apps. No additional setup.

Merchants receive funds in fiat if they choose. No exposure to crypto volatility. Payment Service Providers integrate once and unlock an entire ecosystem. Everything else happens in the background.

How the Experience Actually Feels from a user perspective the process is almost invisible.

At checkout a payment request appears. This can be a QR code a link or a tap-to-pay interaction.

The user opens their wallet.

Why Merchants Will Switch

Merchants are motivated by utility, not ideology. Traditional card networks often impose 2–3% fees, slow payouts, and chargeback risks. WalletConnect Pay offers:

- Faster settlement times

- Lower transaction costs

- No exposure to price volatility

- A familiar checkout experience

These advantages make adoption in 2026 not just likely but inevitable.regulators. As a result crypto payments often worked only in controlled environments or experiments.

All key details are already prepared:

- Amount

- Asset options

- Network routing

No manual input. No confusion. One confirmation.

Transaction completes.

That’s it.

No switching networks. No guessing gas fees. No failed attempts due to wrong chains.

This is where the real innovation lies. Not in complexity but in removing it.

The $33 Trillion Breakthrough: What Stablecoins Actually Fixed

Stablecoins addressed one major problem: price stability. Once a digital dollar reliably stayed close to one dollar it became usable for:

- Cross-border transfers

- Treasury operations

- B2B settlement

- Remittances

This explains the rapid growth in transaction volume. The data cited by Bloomberg shows that most of this activity is not speculative trading. It increasingly resembles real financial and settlement behavior, especially in regions with currency instability or inefficient banking systems.

However stablecoins alone did not solve the checkout experience. Merchants still faced fragmented wallets, different blockchains, varying standards, and unclear regulatory exposure. Consumers still had to make technical decisions they should never need to make during a payment.

What Happens Behind the Scenes

While the user experience is simple, the underlying system is highly structured.

Before a transaction completes, several processes occur automatically:

- Balance verification

- Optimal routing selection

- Optional swaps or bridging

- Compliance screening (where required)

All of this is handled without interrupting the user flow.

Settlement happens on-chain, often near-instant on high-performance networks like Polygon, Base, and others.

Merchants receive predictable outcomes. Users get speed and clarity.

Physical Payments: The Missing Link

Online payments are only part of the equation.

Real adoption requires presence in physical retail.

This is where WalletConnect Pay expands further through partnerships with global POS providers like Ingenico and iMin.

These integrations bring crypto payments directly to physical terminals across millions of locations worldwide.

At a store, the process looks familiar:

- Scan QR or tap

- Confirm in wallet

- Payment completes

No cards. No intermediaries. No additional friction.

WalletConnect Pay: The New Standard for Web3 Commerce

Scaling payments is an art of invisible coordination. That is exactly what WalletConnect Pay was built to do. Think of it as the ultimate upgrade to the world’s financial plumbing. It handles the messy parts of payments that blockchains were never built for.

By standardizing how Web3 wallets and merchants interact it transforms clunky cryptocurrency transactions into a sleek 2-second experience.

- No new hardware for merchants.

- No confusing steps for users.

- Just scan approve and continue.

It is the seamless future of Web3 payments ready for the real world today.

This bridges the gap that crypto has struggled with for over a decade.

The Economic Flywheel

The system works because it aligns incentives across all participants.

For users:

- Self-custody remains intact

- No need for new tools

- Ability to spend existing assets

- Potential rewards and incentives

For merchants:

- Lower fees compared to cards

- Faster settlement

- Access to global crypto-native customers

- No requirement to hold crypto

For PSPs:

- New revenue streams

- Seamless integration into existing systems

- Compliance-ready infrastructure

For wallets:

- Expanded utility

- Increased engagement

- New monetization paths

Each participant benefits without added complexity.

That creates a compounding network effect.

Scale and Infrastructure

WalletConnect Pay is not built in isolation.

It sits on top of WalletConnect’s existing network:

- 700+ wallets

- 500M+ users

- Tens of thousands of applications

The Ingenico Integration

WalletConnect Pay has integrated with Ingenico unlocking stablecoins payments on 40 million terminals across 120+ countries. Suddenly crypto is available at your local grocery store gas station and hotel.

It works on existing Android terminals. Merchants don’t need new hardware they don’t have to hold digital assets and customers get the exact same checkout experience they already know. This is the moment cryptocurrency leaves the digital bubble and enters everyday commerce.

Why Merchants Will Actually Switch in 2026

Merchants don’t care about blockchain they care about fast settlement and ease of use. Traditional card networks often bleed businesses with 2–3% fees, agonizingly slow payouts and chargeback risks. WalletConnect Pay flips this by offering an upgrade that actually solves the problem for everyone.

WalletConnect Pay offers:

- Faster settlement times.

- Lower transaction costs compared to traditional processors.

- No exposure to market price volatility

- A checkout experience customers already understand.

These factors matter more to merchants than the underlying technology.

Incentives for Adoption

To accelerate growth, WalletConnect has proposed a 50 million WCT token incentive program. Consumers can earn up to 2% rewards on purchases, with eligibility covering transactions up to $100,000 per month. Rewards are paid directly to the wallet used at checkout, creating a Web3-native version of cashback.

For the initial launch period:

- Consumers can earn up to 2% in WCT rewards.

- Eligibility covers transactions up to $100,000 per month.

- Available for both online and in-store purchases.

- Rewards are paid directly to the wallet used at checkout.

The Bigger Picture

Crypto has already proven its ability to store value and transfer it globally.

What remained unsolved was usability at scale.

WalletConnect Pay addresses that gap directly.

It doesn’t try to replace existing systems overnight.

It integrates with them.

It doesn’t force users to learn new behaviors.

It simplifies existing ones.

And most importantly, it removes the invisible friction that has held adoption back.

Final Thought

The future of crypto payments will not look like crypto.

It will look like normal payments.

Fast. Simple. Invisible.

But underneath, the infrastructure will be entirely different.

More efficient. More open. More global.

WalletConnect Pay is one of the first systems to make that transition real.

Not as a concept.

But as a working layer of the financial internet.

And once payments become this seamless, adoption is no longer a question.

It becomes inevitable.

Winning on Utility Not Just Ideology

To go mainstream, a payment system needs to be invisible and rewarding. WalletConnect Pay delivers exactly that by merging a standardized payment layer with usage based incentives. It eliminates friction for the merchant and creates value for the user. It creates the ultimate condition for scale: a system where cryptocurrency finally wins on practical terms.

What’s Next: Adapting to the Real World

The roadmap from here is focused on scale: pushing integration through global payment providers and making stablecoins the default choice at checkout. For a decade, the industry tried to force the real world to adapt to the blockchain. WalletConnect Pay finally adapts the blockchain to the real world.

The infrastructure is ready. One day, when you visit your nearest grocery store, you won’t have to ask, Do you accept Amex?” You can just ask, “Do you accept digital currency?” and the answer will be a definite yes.

Redefining Risk Management: Why the Outlook is Bullish

In the world of Web3 security is usually the biggest concern. WalletConnect Pay solves this by keeping assets non-custodial meaning users never hand over their private keys during a transaction. For merchants the risk of market volatility is completely eliminated through instant stablecoin settlement. By removing these two major barriers, the network isn’t just managing risk it is building the most secure foundation for the 2026 economy making the long-term growth potential undeniable.

The Outlook

For years the industry tried to force the real world to adapt to blockchain. WalletConnect Pay flips the script adapting blockchain to the real world. With stablecoins now powering trillions in settlement volume and merchant adoption accelerating, the outlook for Web3 payments is bullish.

Soon, asking “Do you accept digital currency?” at checkout will be as natural as asking about Visa or Mastercard.

Frequently Asked Questions (FAQ)

Q: How is this system different from standard apps like Google Pay? A: Unlike traditional apps that rely on banks, this new infrastructure uses decentralized networks. This cuts out the middleman, allowing for faster processing and lower fees without needing a credit card processor.

Q: Do I need a special app to spend digital assets? A: You likely won’t need a separate app. The goal is to integrate directly with the wallets you already use, making the checkout process as simple as scanning a QR code at the counter.

Q: Is it safe to use these assets for daily shopping? A: Yes. Because the system uses value-pegged assets (like digital dollars), it avoids the wild price swings usually associated with market trading. Your buying power remains consistent during the transaction.

Q: Where can I check the market data for these coins? A: You can view volume and market caps on major tracking platforms. As adoption grows, these sites are now listing real-world utility data alongside standard trading charts.

Q: Do stores need new machines to accept this? A: No. Through strategic partnerships, shops can use their current Android terminals. They receive the money in their local currency, so they don’t have to manage any complex digital wallets themselves.